Welfare fraud prevention is all about the proactive systems and smart measures agencies put in place to stop people from illegally getting public assistance. The whole idea is to catch fraudulent claims before any money goes out the door, rather than trying to claw it back later. This protects public funds and, more importantly, makes sure help gets to those who genuinely need it.

The Urgent Need for Modern Fraud Prevention

Let's be blunt: the old "pay-and-chase" model for dealing with welfare fraud is broken. For decades, agencies have been stuck in a reactive cycle, only finding overpayments or outright fraud months, or even years, after the fact. This isn't just inefficient; it’s a massive drain on public resources and it chips away at the public's trust in the very systems meant to be a safety net.

As public assistance programs move more services online, the doors open wider for more sophisticated fraud. We've moved past simple income misreporting. Today’s threats are much more complex, from organized crime rings exploiting system vulnerabilities to AI-powered scams that can create fake identities on a massive scale.

This guide is about leaving those outdated, reactive methods behind. It’s a roadmap for building a proactive, modern defense against fraud. The goal is to fundamentally shift your focus from chasing losses to preventing them from ever happening.

Moving Beyond Reactive Measures

Taking a proactive stance is absolutely essential for maintaining the integrity of social benefit programs. It’s about building a framework that can see threats coming and neutralize them before they can cause any financial harm. This takes a multi-layered strategy that weaves together technology, data, and close collaboration.

Some of the key pillars of a truly modern prevention strategy include:

- Data Analytics: Using powerful tools to connect the dots between different data sources and spot suspicious patterns before an application ever gets approved.

- Tougher Identity Verification: Putting strong checks in place right at the application stage to block bad actors—like those using stolen or fake identities—from ever getting into the system.

- Powerful Partnerships: Creating a united front by sharing intelligence between government agencies and with private sector partners, like banks and other financial institutions.

- Continuous Monitoring: Routinely checking recipient eligibility to catch any changes in circumstances that might lead to overpayments or fraud down the line.

The core idea is simple but incredibly powerful: Make it extremely hard for fraudsters to get through, while making the application and benefit process smooth and easy for legitimate families and individuals.

This isn't just about saving taxpayer money, though that's a huge benefit. It's about preserving the integrity of and public trust in these essential programs. When you get ahead of fraud, you ensure that vital resources are protected and go directly to the people who truly need them. You end up building a stronger, fairer, and more efficient system for everyone involved.

Using Data Analytics to Proactively Detect Fraud

What if you could stop fraud before a single dollar is ever misspent? That's not some futuristic fantasy; it’s what happens when you build a solid, data-driven framework. The real power comes from connecting data sources that rarely talk to each other—things like tax records, employment data, and immigration status—to spot red flags almost instantly. This is a fundamental shift, moving from reacting to losses to proactively preventing them in the first place.

Instead of just chasing down fraud after the fact, agencies can now anticipate and shut down threats before they have a chance to grow. It’s all about creating an intelligent system that learns and adapts. This isn't just a theory, either. Public organizations around the world are using advanced analytics to cross-reference multiple data sources, catching inconsistencies long before any benefits are paid out.

Unifying Disparate Data Sources

The first real step is to break down the information silos. Fraudsters absolutely love it when information is scattered and disconnected. When you unify data from different agencies and departments, you get a 360-degree view of an applicant or recipient, making it incredibly difficult for discrepancies to hide.

Think about the key data streams you can tap into:

- Employment and Wage Records: Does the income reported on an application match what state and federal employment databases show? This is a basic but powerful check.

- Tax Information: You can confirm household size and declared income by matching application details against official tax filings.

- Public Records: Property deeds, business registrations, and vehicle records are great for uncovering assets that someone might not have mentioned.

- Criminal Justice Data: Is an applicant currently incarcerated or facing outstanding warrants that might affect their eligibility? This data can tell you.

- Vital Records: Using birth, death, and marriage certificates is crucial for verifying identities and relationships, which helps stop identity theft cold.

Connecting these dots creates a powerful web of verification that’s tough to beat. If your organization is just starting out, it’s helpful to see how others have done it. For a great example, you can review this case study on https://unify.scholarfundwa.org/case-study/data-analytics-for-nonprofits to see how they harness data for better outcomes.

From Red Flags to Risk Scores

Once all your data is connected, you need to make it do something. This is where predictive analytics and risk-based scoring come into play. Instead of giving every single application the same level of scrutiny, you can assign a risk score based on a combination of different factors.

A low-risk application? It can be fast-tracked for approval. But a high-risk one gets flagged for a human case manager to review. This puts your expert resources right where they're needed most. A classic example is seeing dozens of separate benefit claims all coming from a single residential address—a risk-scoring model would flag that immediately. Another is an applicant whose details are suspiciously similar to a profile from a previously confirmed fraud case.

The goal here isn't to automatically deny benefits. It's about ensuring due diligence. A high risk score is simply a trigger for a closer look, which protects the program’s integrity while making sure people who genuinely need help get it without unnecessary hold-ups.

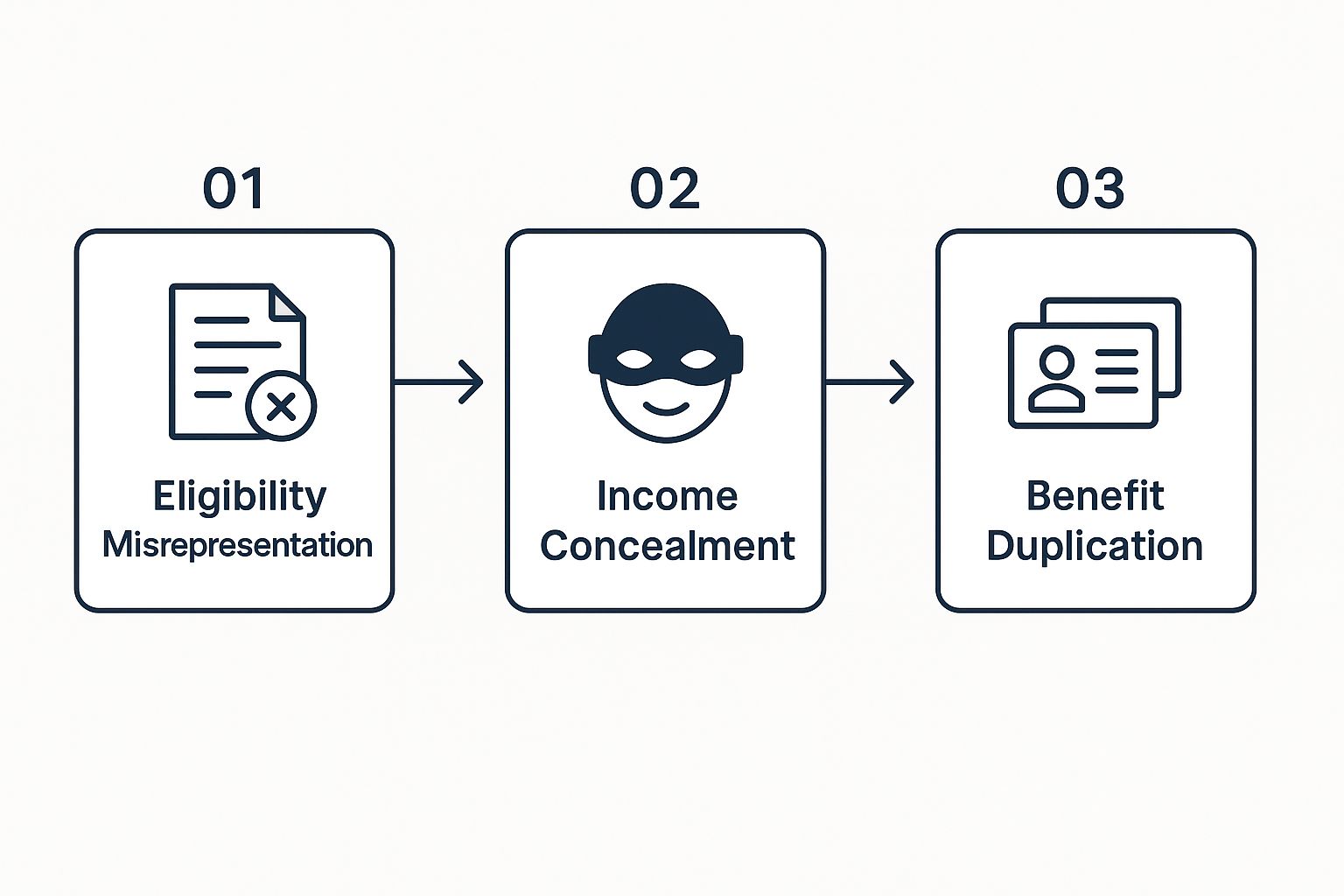

The infographic below shows some of the most common types of fraud that data analytics can help you zero in on.

As you can see, this process helps target specific schemes, whether it's someone misrepresenting their eligibility, hiding income, or trying to claim duplicate benefits from different programs.

For any of this to work, though, an organization has to truly embrace a culture of data-driven decision-making. Getting those insights from analytics is one thing; turning them into action is another. For anyone looking to build that mindset, mastering data-driven decision making is a fantastic resource.

Implementing Practical Analytics Techniques

Building a data analytics program from scratch can feel daunting, but it doesn't have to be an all-or-nothing project. You can start with simpler techniques and gradually work your way up to more advanced models as your team gets more comfortable and you secure more resources.

To get started, it helps to understand some of the core methods. Here’s a quick look at a few powerful techniques and how they're used on the ground.

Key Data-Driven Fraud Detection Techniques

By bringing these techniques into your workflow, you can shift from a defensive game of catch-up to an offensive strategy that stays one step ahead. It’s the best way to protect public funds and, just as importantly, reinforce the community’s trust in these vital support systems.

Strengthening Your First Line of Defense: Identity Verification

Think of your application process as the front door to your agency. If that door has a flimsy lock, your entire system is at risk. Fraudsters are experts at finding weak entry points, and once they're in, the damage is done. That’s why modern welfare fraud prevention starts right here, with robust, multi-layered identity verification.

The game has changed. We're no longer just dealing with crudely forged documents. Today's threats are far more sophisticated, from synthetic identities—cleverly assembled from both real and fake information—to large-scale identity theft rings.

Implementing Modern Verification Methods

To stand a chance against these advanced tactics, your verification process has to be just as advanced. Simply asking for a Social Security number and an address won't cut it anymore. The real challenge is building a system that’s ironclad for fraudsters but still smooth and easy for the genuine applicants who depend on you.

Here are a few essential technologies that should be part of any modern identity verification strategy:

- Multi-Factor Authentication (MFA): This is a simple but incredibly effective method. It just means a user has to prove their identity in more than one way, like entering a password and then a one-time code sent to their phone.

- Biometric Verification: Using unique human traits like a facial scan or a fingerprint provides an exceptionally high level of confidence. This approach is a powerful weapon against synthetic identity fraud, where other data points might look legitimate.

- Digital Identity Services: These platforms are a game-changer. They can instantly cross-reference an applicant's details against thousands of public and private databases, validating their identity in real time.

The need for these measures isn't just theoretical; it's urgent. Projections show that cybercrime—which includes the fraud, identity theft, and data breaches we're fighting—is on track to cost the world $10.5 trillion annually by 2025. That's a staggering number that puts our social programs directly in the crosshairs. You can get a deeper dive into these trends in the 2025 Identity Fraud Report from Entrust.

The Rise of AI in Document Verification

Even with all these digital checks, we still rely on documents like driver's licenses and birth certificates. The problem? The human eye is no longer a reliable tool for spotting today’s sophisticated fakes. This is where Artificial Intelligence (AI) has become an indispensable part of welfare fraud prevention.

AI-powered verification can scan an uploaded document in seconds, looking for signs of fraud that are completely invisible to a caseworker.

AI doesn't just check if the name on a document matches the application. It analyzes pixel density, font consistency, hologram placement, and metadata to detect subtle signs of digital alteration or forgery.

This technology can catch everything from a slightly altered pay stub to a professionally crafted deepfake ID. By integrating these tools, you stop fraudsters at the very beginning—before they ever get a foothold in your system. This kind of tech is a core part of any effective social services technology platform.

Balancing Security with Accessibility

I hear this concern all the time: "Won't all this new security make it harder for the people who actually need our help?" It's a fair question. The key is to design a system that is both secure and flexible.

You don't have to force everyone down the same path. An agency could, for instance, offer multiple ways to verify an identity. Someone comfortable with a smartphone can use a quick facial scan. Another person might prefer a video call with a case manager or even an in-person visit. The goal is to provide choices that respect different comfort levels and technological access.

At the end of the day, strengthening your identity verification isn't about building an impenetrable fortress. It’s about building a smarter front door that knows how to welcome friends and spot strangers. By layering modern solutions like MFA, biometrics, and AI-powered document analysis, you can drastically cut your vulnerability to fraud while still offering a dignified, user-friendly experience to the people you’re there to serve.

Building a United Front Through Collaboration

Fraudsters don’t see walls between agencies—they see opportunities. They count on the fact that the Department of Labor isn't talking to the Social Services office, and that neither is in constant communication with the banks handling the payments. To truly get ahead of welfare fraud, we have to tear down those silos and start working together.

https://www.youtube.com/embed/RmoWn3yONw8

An isolated defense is a recipe for failure. When agencies and private sector partners build a collaborative ecosystem, the entire system becomes more resilient. It creates an environment where it's just too difficult and too risky for criminals to operate. This starts with breaking down the data barriers that have traditionally kept government departments from sharing what they know.

Even more importantly, it means building strong public-private partnerships. Financial institutions are on the front lines. They see the money move, making them indispensable allies in flagging suspicious transactions that an agency, working alone, might never catch.

Forging Strong Inter-Agency Alliances

Before looking outside, the first step is to get your own house in order. It's surprisingly common for a state’s housing authority, labor department, and social services agency to run on completely separate systems. There’s often little to no data sharing, which is a dream scenario for a fraudster.

Think about a classic scheme: someone claims unemployment benefits while also getting disability assistance from a different agency, never reporting the income from either. Without agencies comparing notes, this kind of double-dipping can go unnoticed for years, costing taxpayers a fortune.

To shut this down, many regions are forming dedicated welfare fraud task forces. These groups are a game-changer, bringing investigators and data analysts from different departments to the same table. Their mission is to:

- Share intelligence: Regularly exchange information on new fraud schemes and suspicious activity.

- Run joint investigations: Combine resources and expertise to tackle complex cases that cross jurisdictional lines.

- Build shared data platforms: Create secure systems where authorized staff can cross-reference applicant data from multiple sources in real time.

This approach closes the gaps that criminals rely on. A red flag in one system instantly becomes a red flag for everyone.

The Power of Public-Private Partnerships

While getting government agencies to talk to each other is a huge step, the strongest defense brings in the private sector. Banks and credit unions have a unique view into potential fraud because they see the actual flow of benefit payments.

A partnership with a bank can turn a simple direct deposit into an active security measure. If a single bank account suddenly starts receiving benefit payments for dozens of different individuals, that's a massive red flag for an organized fraud ring.

This type of collaboration is becoming more than just a best practice; it's becoming a necessity. We're seeing a major shift where collaboration and regulatory accountability go hand-in-hand. There’s a growing focus on ‘failure to prevent’ initiatives, putting more pressure on all institutions to invest in better fraud detection. This is fostering a culture of vigilance that ultimately protects the public purse. You can learn more about these fraud prevention trends and what they signal for the future.

When a welfare agency and a bank work together, they can spot and shut down these schemes almost instantly. The agency provides the program context, and the bank provides the real-time financial data. It's a powerful combination.

Creating an Ecosystem of Prevention

Ultimately, the goal isn't just one-off projects or partnerships. It's about creating a dense web of shared intelligence where fraud becomes immediately obvious. This isn't about a single tool; it's about building a culture of constant communication and cooperation.

When government agencies, financial institutions, and even technology providers are all on the same page, they create a truly formidable barrier. This united front sends a clear message to anyone thinking of cheating the system: the gaps are closed, everyone is watching, and the risk is no longer worth the reward.

Using Continuous Monitoring for Ongoing Integrity

The work isn't over once an application is approved. Far from it. Life is dynamic—a new job, a change in who's living in the home, or an unexpected inheritance can all shift someone's eligibility for benefits. In my experience, failing to keep up with these life changes is one of the biggest reasons for overpayments and, ultimately, fraud.

This is exactly why continuous monitoring is so critical. It’s a complete shift away from the old, ineffective "pay-and-chase" model. Instead of waiting for an annual review to catch problems, your system should be built to flag discrepancies as they happen. It’s about maintaining program integrity every single day.

Setting Up Automated Data Checks

At the heart of any solid monitoring program are automated, periodic data checks. These systems work quietly in the background, constantly comparing recipient data against key external sources to spot significant changes. This isn't about invasive surveillance; it's about smart, targeted verification that keeps the program honest.

Think about it. You could set up a system to automatically cross-reference your recipient list with state wage databases every quarter. This one check alone can instantly flag people who may have started a new job or gotten a raise they forgot to report. It's an incredibly powerful tool for preventing fraud before it takes root.

Some of the most valuable data sources to integrate are:

- Employment and Income Databases: To catch new or unreported earnings.

- Vital Records: For changes in marital status or household composition.

- Residency and Property Records: To confirm a recipient still lives where they claim and hasn't acquired major assets.

- Incarceration Data: To identify individuals who become ineligible if they are incarcerated.

By automating these checks, you stop bogging down your caseworkers with tedious manual verifications. They can then focus their expertise on the complex cases that truly need a human touch.

Using Intelligent Alerts for Proactive Intervention

Data is useless without action. The next logical step is to build an intelligent alert system that notifies case managers about potential issues before they spiral out of control. When the system finds a mismatch—like reported income not lining up with state wage data—it should automatically generate an alert.

An alert isn't an accusation. It's simply a signal for a caseworker to follow up, ask questions, and get the full story. It’s an opportunity for proactive intervention, not immediate punishment.

For instance, an alert might get triggered if a recipient’s EBT card is suddenly used in another state for several weeks. This could mean they've moved without telling you, or it could have a perfectly good explanation. The alert gives the caseworker a reason to check in, preventing a small overpayment from snowballing into thousands of dollars over months. This kind of proactive approach is a core principle of good risk management, a topic explored further in this guide to https://unify.scholarfundwa.org/case-study/nonprofit-risk-management.

Ensuring Fair and Evidence-Based Enforcement

When an investigation does confirm fraud, your enforcement must be firm, fair, and consistent. The goal is twofold: recover any lost funds and create a credible deterrent that discourages others. Crucially, this entire process has to respect an individual's right to due process.

The investigation needs to be methodical and built on solid evidence. This means carefully collecting and documenting all relevant information, conducting professional interviews, and making sure every conclusion is backed by undeniable facts. The principles here aren't unique to welfare; you can find similar thinking in the advanced methods and strategies for uncovering corporate fraud.

Once fraud is confirmed, the consequences should fit the crime. Actions can range from benefit disqualification and mandatory repayment plans to, in the most serious cases, criminal prosecution. By pursuing meaningful consequences, agencies send a powerful message that fraud has real costs—strengthening the integrity of the entire system for the people who truly need it.

Answering Your Top Questions on Fraud Prevention

When agencies start upgrading their fraud prevention systems, a lot of good questions and valid concerns pop up. Whether you're a program manager on the front lines or a policymaker shaping the rules, you need straight answers. Let's dig into some of the most common questions we hear.

What Is Legally Considered Welfare Fraud?

At its heart, welfare fraud happens when someone intentionally provides false information or hides the truth to get public assistance they aren't actually eligible for. It's more than just an honest mistake; it's a deliberate act of deception.

Think of it in these common scenarios:

- Hiding Income: Not reporting money from a job, a side hustle, or other sources.

- Misrepresenting Your Household: Claiming dependents who don't live with you or failing to report when someone moves out.

- Falsifying Documents: Creating fake pay stubs or rental agreements to appear eligible.

- Benefit Trafficking: A particularly serious form is selling or trading SNAP benefits (often called food stamps) for cash.

The key word is always intentional. People make honest mistakes, and that's different. Fraud is about a calculated effort to game the system for personal gain. This is why agencies run data checks and eligibility reviews—to catch those discrepancies and ensure funds go to those who truly qualify.

Will Stronger Security Exclude People in Need?

This is probably the most critical question we get, and the answer comes down to smart, thoughtful design. The point of a modern fraud prevention program isn't to build walls; it's to create a more secure, streamlined path for the people who legitimately need help. You want to be tough on fraud, not on families.

The best systems strike a delicate balance between robust security and genuine accessibility. A high-tech solution that blocks eligible people is a failure, no matter how much fraud it stops. True success is a system that is both secure and inclusive.

So, how do you get there? It’s not about choosing one over the other.

- Provide different ways to verify identity. Someone might be perfectly happy doing a quick facial scan on their smartphone. Another person might feel more comfortable with an in-person visit or a video call with a caseworker. Offer both.

- Use risk-based reviews. Instead of putting every single applicant through the most intense scrutiny, use data to flag only the high-risk applications for a closer look by a human. This lets you fast-track approvals for the vast majority of people who are clearly eligible.

- Offer clear instructions and real support. Things like multilingual guides, simple application forms, and easy-to-reach help desks make sure technology serves people, rather than becoming another hurdle.

When you implement strategies like these, you can make it incredibly difficult for fraudsters while actually making the process smoother and faster for everyone else.

What Happens if an Overpayment Is a Mistake?

Honest mistakes and intentional fraud are two very different things, and they should be handled that way. An overpayment is simply when a recipient gets more benefits than they were supposed to, often because of a simple error or an unreported change—like getting a pay raise or a child moving out.

When an overpayment is discovered and it looks like an honest mistake, the focus is on recovery, not punishment. The process usually looks something like this:

- Notification: The agency will reach out and let the person know about the overpayment, explaining the amount and why it happened.

- Repayment Plan: From there, they'll work with the individual to set up a reasonable repayment plan. This might mean a small deduction from future benefits or a monthly payment that fits their budget.

Communication is everything. If a recipient realizes they made a mistake on their application or their situation changed, they should report it right away. That kind of transparency goes a long way in showing there was no intent to defraud the system, making the whole resolution process much less stressful.

How Can Agencies Ensure Privacy with Data Sharing?

Worries about data privacy are 100% valid, especially when you're talking about agencies sharing information. Protecting personal data isn't just a good idea; it's a non-negotiable part of the process. A modern approach to preventing welfare fraud is built on handling data securely and ethically.

Agencies have to follow strict rules to get this right:

- Anonymized Data: For spotting big-picture trends, data can be anonymized or grouped together. This lets analysts find fraud patterns without ever looking at individual identities.

- Role-Based Access: Not everyone in an agency needs to see everything. Sensitive data is locked down, and access is given only to specific staff members with a legitimate reason to view it.

- Secure Data Exchange: Any information that's shared between agencies moves through encrypted, secure channels to prevent it from ever being intercepted.

- Legal Frameworks: Data sharing doesn't happen in a vacuum. It's governed by strict legal agreements, like a Memorandum of Understanding (MOU), that spell out exactly what data can be shared, with whom, and for what specific purpose.

The goal isn't to create a giant, open database of everyone's personal information. It's about running specific, targeted data checks to verify eligibility—and that’s it. This focused approach protects privacy while still making sure the program has integrity.

Ready to build a system that combines robust security with seamless delivery? Unify by Scholar Fund provides the tools you need to design, manage, and scale your assistance programs effectively. Our platform automates payments, ensures compliance, and offers the real-time analytics necessary for modern welfare fraud prevention, all while putting the applicant experience first. Learn more about how you can deliver funds faster and smarter.

View more case studies

Powering Benefit Programs at Scale