Picture this: you need to send a critical package across the country. Using traditional banking is a bit like using standard mail—it’ll get there, but it takes a few business days and follows a strict schedule. Instant payment processing, on the other hand, is like hiring a dedicated courier who delivers your package directly, in minutes, any time of day or night. That’s the level of speed and reliability we're talking about.

What Exactly Is Instant Payment Processing?

At its heart, instant payment processing allows money to move from one bank account to another and be available for use almost immediately. This is a huge leap from older systems like ACH (Automated Clearing House), which group payments together and process them in batches. With instant payments, there are no batch delays, no frustrating holds, and no waiting for the next business day.

Think of it as a dedicated, always-open highway between bank accounts. When you send money, the network verifies the account details, checks for sufficient funds, and finalizes the transaction all in one go, usually within seconds. This leads to payment finality, which is a game-changer. It means that once the money is sent, it’s truly sent—it can't be clawed back or reversed. That certainty builds a tremendous amount of trust for everyone involved.

Shifting Financial Habits

We're seeing a massive global shift away from physical cash and toward digital everything. In fact, over 70% of consumers worldwide now use some form of digital payment, a trend that's especially pronounced in growing economies. This whole movement is being supercharged by mobile wallets and national payment infrastructures, with the global payment processing industry projected to hit $139.9 billion by 2030.

This isn't just about convenience; it's a fundamental rewiring of how economies work. Even specialized areas like digital currencies are moving into the mainstream, forcing us all to start demystifying crypto payment processing and adapting to new financial tools.

The real magic is in the 'settlement.' A traditional payment might show up as 'pending' in your account for days, but an instant payment settles right away. The money is actually there and ready for you to use.

To really nail down the difference, let’s look at them side-by-side.

Instant Payments vs. Traditional Payments at a Glance

The table below breaks down the core differences between instant payment processing and conventional methods like ACH. It clearly shows why instant payments are the superior choice for speed, availability, and certainty.

For any organization managing time-sensitive funds, like cash assistance programs, the advantages are undeniable. The comparison makes it obvious which system is built for the modern world.

How Instant Payment Networks Move Money

To really get a feel for how instant payments work, it helps to peek behind the curtain at the technology making it all possible. Think of an instant payment network as the financial world's central nervous system—a sophisticated system designed to process information and execute commands 24/7, all in the blink of an eye. This is what turns the promise of immediate fund transfers into a reality.

At the heart of it all are central clearing houses, which operate a bit like air traffic control for money. In the United States, the big players are The Clearing House's RTP® network and the Federal Reserve's FedNow® Service. They don’t just shuffle money from one place to another; they conduct the entire transaction from start to finish in one smooth, continuous process.

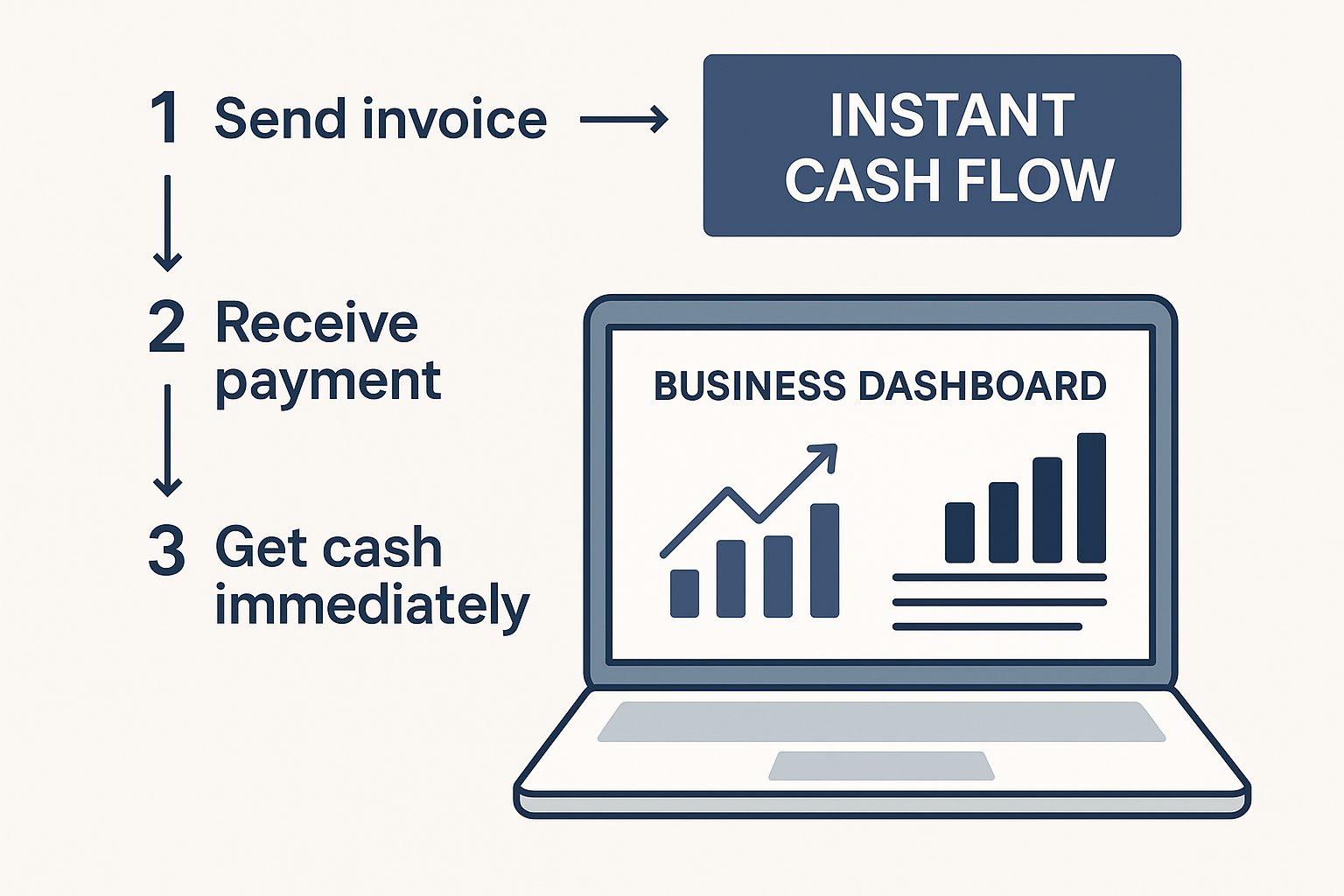

This image gives you a sense of how organizations can track this real-time flow of cash through a modern dashboard.

As you can see, the right platform gives you immediate visibility into every transaction, putting real-time financial oversight right at your fingertips.

A Step-by-Step Look at the Transaction

When someone initiates a payment, the money doesn't just get shot into the digital ether. Instead, the network kicks off a complex verification and confirmation dance that happens in just a few seconds.

Here’s a simple breakdown of what that journey looks like:

- Initiation: It all starts when the sender—whether an organization or an individual—tells their bank or payment provider to send money. This instruction is sent as a message to the instant payment network.

- Verification: The network immediately pings the recipient's bank. That bank then checks to make sure the account details are correct, the account is open, and it's able to receive the funds.

- Confirmation: Once everything checks out, the recipient's bank sends a confirmation message back through the network, giving the green light.

- Clearing and Settlement: With confirmation in hand, the network clears the transaction and settles the funds between the two banks at the same time. The money is then officially credited to the recipient's account.

This whole sequence is over almost as soon as it begins. The funds aren't just sent; they are immediately available for the recipient to use. This is a massive departure from older systems that clump payments together and process them in batches, which is why they take so much longer.

The most important concept to grasp here is payment finality. Once an instant payment lands in the recipient's account, it's done. It's final and irrevocable. This completely removes the risk of a payment getting clawed back days later, giving both the sender and the receiver total certainty and trust in the transaction.

It's Not Just About Speed—It's About Data

What truly powers these networks is a sophisticated data messaging standard, typically ISO 20022. You can think of it as a universal language for financial information. It allows a ton of data to travel with the payment, like invoice numbers, remittance details, or specific program identifiers.

This is a game-changer for organizations managing large-scale cash assistance. Instead of a vague line item on a bank statement, each payment arrives with its full context. This makes tracking, reporting, and reconciliation incredibly straightforward, cutting down on administrative headaches and boosting transparency for everyone involved. The end result is a financial system that's not just faster, but much, much smarter.

The Global Shift to Real-Time Payments

The move toward instant payment processing isn't just a minor tweak to the financial system—it's a massive, worldwide revolution. All across the globe, countries are rolling out powerful real-time payment networks, driven by a combination of consumer demand for speed and government pushes for economic modernization. This isn't just about getting your money faster; it's about fundamentally rewiring how economies work and bringing millions of people into the digital age.

The adoption is happening at an incredible pace. We're seeing instant payments go from a nice-to-have feature to the absolute standard. This is setting a new expectation for how money should move in the 21st century: instantly, securely, and with total transparency.

The Powerhouses of Instant Payments

To really grasp the impact, you just need to look at a few international success stories. These countries show what's possible when you build a system that works for everyone, achieving incredible adoption rates and sparking major economic change in just a few years.

- India's UPI (Unified Payments Interface): This is probably the best-known example. UPI brought hundreds of millions of people—from small street vendors to rural farmers—into the digital economy almost overnight. It made sending and receiving money ridiculously simple.

- Brazil's PIX: Launched in late 2020, PIX was embraced by over 70% of the country's adult population in record time. It's now the go-to payment method for everything, proving just how much people want financial tools that actually work for them.

These systems teach us a powerful lesson: if you make a payment method simple, safe, and instant, people won't just use it—they'll flock to it. This creates a network effect that quickly leaves slower, clunkier financial systems in the dust.

Growth by the Numbers

The numbers backing this global movement are staggering. In 2022, instant payments already accounted for 13% of all non-cash transactions worldwide. That share is expected to jump past 22% by 2028. The total number of transactions hit an astonishing 195 billion in 2022 and is on track to blow past 500 billion a year by 2027.

This explosive growth is powered by national systems like India's UPI, which now handles billions of transactions every single month, and Brazil's PIX, which processed over 41 billion transactions in 2023 alone.

This isn't just a phenomenon in developing nations, either. Developed economies are catching up fast, with major infrastructure projects like the Federal Reserve's FedNow Instant Payments System coming online. For any organization that delivers cash assistance or manages large-scale benefit programs, the message is crystal clear. Getting on board with instant payments is no longer a strategic option—it’s an absolute necessity to stay relevant and effective.

What Are the Real-World Benefits for Your Organization?

Let's move past the technical jargon. What does instant payment processing actually do for you and the people you serve? For recipients, the answer is simple but powerful: they get the money they need, right when they need it. This can be a lifeline that eases financial stress, covers an unexpected emergency, and builds a real sense of security.

But the advantages for the organizations delivering this aid are just as profound. Switching to an instant model triggers a ripple effect of positive changes, transforming how you operate, manage your money, and connect with your community. It’s a move away from slow, old-school methods toward a far more dynamic and responsive system.

Boost Your Operational Efficiency

One of the first things you’ll notice is the end of clunky, traditional payment methods. Just think about all the time and resources that go into printing, stuffing, and mailing physical checks. Every single one of those steps adds delays, costs, and opportunities for things to go wrong, from mail getting lost to a simple typo in an address.

Instant payments cut right through all that. With just a few clicks, funds land directly in a recipient's account, saving your team countless hours of manual work. This frees up your staff to focus on what really matters—your mission—instead of getting bogged down in payment logistics. Seeing this in action can be a game-changer, as detailed in this case study on nonprofit payment processing.

By automating disbursements, organizations can slash the time it takes for aid to get into someone's hands. A process that used to drag on for weeks can now be wrapped up in hours, or even minutes.

Gain Better Control Over Cash Flow and Finances

Real-time transactions give you a much clearer picture of your organization's financial health. With traditional batch payments, there's always a lag. You send the money out, but then you’re left waiting and wondering when it will actually clear, creating a fog of uncertainty around your cash flow.

Instant payments provide immediate settlement and confirmation. You know the exact status of every dollar in real time, which gives you incredible control over your organization's liquidity. This shift does mean taking a fresh look at your internal processes, especially how you handle bank reconciliation statements, to keep up with the speed of the data.

Build Trust Through Speed and Transparency

At the end of the day, speed and transparency are the building blocks of trust. When recipients get their funds instantly, it shows them your organization is reliable and can deliver on its promises. No more waiting, no more worrying.

This direct, dependable delivery method has a massive impact on your relationship with the community you serve. Imagine a nonprofit sending out emergency aid after a natural disaster. Being able to get funds to families within minutes of confirming their need doesn't just provide critical relief—it proves your organization is effective, responsive, and truly committed to its mission.

Navigating Security in a High-Speed World

When money moves in seconds, security has to be more than just an afterthought—it needs to be built into the very fabric of the system. While instant payment processing is all about speed, a modern platform is designed with multiple layers of defense to protect every transaction from the moment it’s sent to the moment it’s received. This ensures that speed never comes at the expense of safety for your organization or the people you serve.

Think of it like a digital fortress. The outer walls are end-to-end encryption, a process that scrambles all the data so it's completely unreadable to anyone who isn't supposed to see it. Then, inside the walls, another process called tokenization replaces sensitive details like bank account numbers with unique, non-sensitive identifiers. So, even if a fraudster managed to intercept the data, they’d be left with a useless string of characters instead of actual financial information.

Built-In Defenses Against Modern Threats

Today's payment platforms don't just wait for threats to happen; they actively hunt for them. Using AI-powered monitoring, these systems analyze transaction patterns in real time to spot anything that looks out of the ordinary. With major processors seeing a 40% increase in non-card payment volume over the last year, this kind of intelligent fraud prevention is more critical than ever.

This proactive stance is your best defense against common schemes like:

- Phishing Schemes: Scams designed to trick recipients into giving up their personal information.

- Account Takeovers: When a criminal gains unauthorized access to someone's account to steal funds.

- Identity Fraud: Using stolen personal data to create fake recipient profiles and divert payments.

The best security is the kind that works tirelessly in the background without anyone noticing. The goal is a smooth payment experience where robust, multi-layered protection is simply part of the process, not something clumsily bolted on later.

Staying Compliant Without the Headache

On top of fighting fraud, organizations also have to deal with a tangle of financial regulations. Rules like the Payment Services Directive (PSD2) and Anti-Money Laundering (AML) laws are there to make payments safer for everyone, but keeping up with them can feel like a full-time job.

This is where a good payment provider proves its worth. They build these compliance checks right into their platform, automatically screening transactions and helping you meet all the necessary legal standards. By taking on the heavy lifting of security and compliance, they free you up to focus on your mission, not on becoming a regulatory expert. It’s all about delivering funds with both speed and complete peace of mind.

Implementing Your Instant Payment Strategy

So, you're ready to bring an instant payment processing system into your organization. Don't think of it as a massive, intimidating overhaul. Instead, see it as building a clear roadmap that guides you from your initial idea all the way to a successful launch. It's all about making smart, deliberate choices that set up both your program and its recipients for success.

The first, and arguably most critical, step is choosing the right payment provider. It's easy to get fixated on transaction fees, but you need to look at the bigger picture. Your ideal partner will offer a platform that's not only secure but can also grow with you. Dig into their security protocols, ask about their capacity for handling larger payment volumes, and, importantly, see how well their system integrates with your existing financial software. A smooth integration is what saves you from data-entry nightmares and reconciliation headaches down the road.

Designing a People-First Process

Once you’ve picked a provider, the spotlight turns to the user experience. You absolutely have to design a simple, intuitive onboarding process for recipients. It doesn’t matter how fast the payment is if people struggle to sign up and receive their funds. Think clear instructions, minimal steps, and a frustration-free experience.

Communication is just as crucial. You need a solid plan for keeping recipients in the loop at every stage. This helps manage expectations and, more importantly, builds their trust in the system.

A great strategy often kicks off with a focused pilot program. Start small. Pick a controlled group of recipients to test your entire workflow from start to finish. This is your chance to gather real feedback, find any rough patches, and smooth them out before you go big.

Integrating Data for Smarter Programs

A truly successful implementation does more than just move money quickly—it generates valuable insights. When you integrate your new payment system with your program management software, you unlock the ability to track disbursements in real time and see what kind of impact they’re having.

For nonprofits, this data is gold. You can use it to fine-tune your approach, improve your programs, and show funders exactly what their support is achieving. To see this in action, check out these key insights on data analytics for nonprofits.

Common Questions About Instant Payments

Even when the benefits are clear, it's natural to have questions about how instant payment processing actually works on the ground. Think of this as the practical "how-to" part of the guide, where we tackle the most common things organizations want to know before they dive in.

How Is This Different From a Wire Transfer?

It’s a common question, since both seem fast. The real difference is in the mechanics and accessibility. Wire transfers are a bit old-school; they’re typically handled by a person at a bank during business hours and can come with some hefty fees.

Instant payments, on the other hand, are completely automated. They run 24/7 on modern networks like RTP® or FedNow® and usually cost a fraction of what a wire transfer does. It’s the difference between mailing a letter overnight versus sending an email—one is a manual process, the other is instant and digital.

Can Instant Payments Be Reversed or Canceled?

The short answer is no, and that’s actually one of its biggest strengths. Once the money hits the recipient’s account, it’s final. It can't be pulled back.

This concept is called "payment finality," and it’s a game-changer for aid delivery.

For someone relying on time-sensitive funds, this finality offers incredible peace of mind. When they see the money in their account, they know it's theirs to use right away. There's no risk of it vanishing later because of a processing delay or insufficient funds on the sender's end.

What Information Do I Need to Send a Payment?

This is where things get much easier than traditional banking. While you can still use the standard account and routing numbers, many platforms have simplified the process significantly.

Often, all you need is a recipient’s email address or phone number. This small change makes a massive difference in how quickly and easily you can get people enrolled in your program and paid.

How Do I Keep My Program Compliant?

This is a major concern for any organization handling money, and rightly so. The good news is that you don't have to become a compliance expert overnight.

Modern, reputable payment platforms build all the necessary compliance tools right into their software. They handle the tricky parts—like identity verification and fraud screening—behind the scenes. This ensures your program operates within financial regulations without adding a huge administrative burden to your team. For groups managing grants, using these digital systems is a core part of today's grant management best practices.

Ready to deliver aid and benefits faster and more efficiently? Unify by Scholar Fund provides the tools you need to design, manage, and scale your cash assistance programs with confidence. Learn how Unify can help your organization.

View more case studies

Powering Benefit Programs at Scale